Trusted Financial Planning Partner

Key Features and Structure

There are two broad categories that encapsulate life insurance products:

Protection policies: Focused on providing pure financial security, typically by offering a lump-sum payment should the insured event occur.

Investment policies: Combine protection with capital growth opportunities, such as savings accounts or investment-linked plans where premiums accumulate value over time.

Insurance contracts invariably include detailed terms, exclusions, and limitations defining liability—most notable exclusions involve fraud, high-risk activities, or suicide within specified periods after purchase.

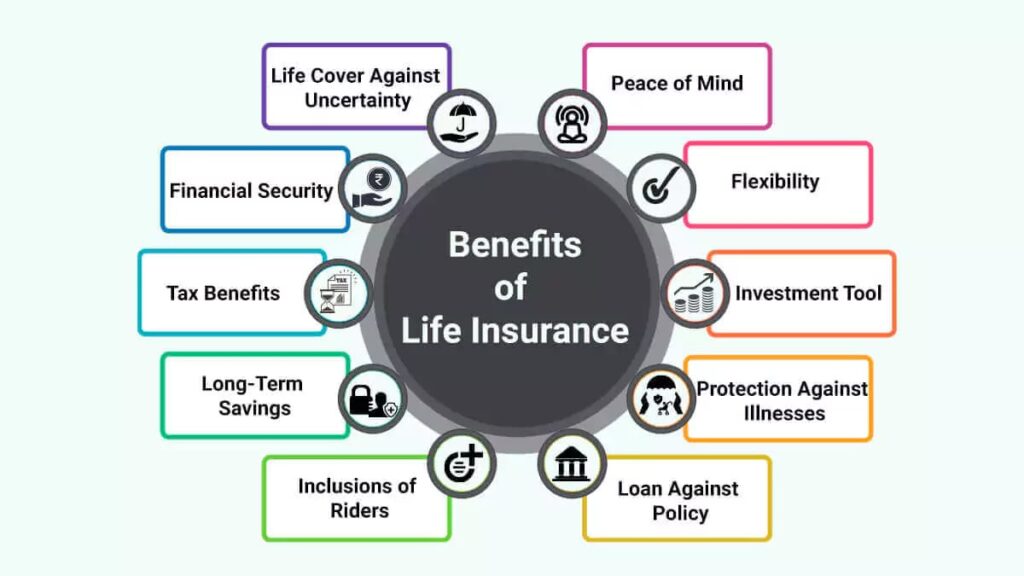

Benefits of Life Insurance

The role of life insurance transcends basic risk cover, contributing to holistic financial planning.

Financial Protection: Life insurance ensures that surviving family members remain financially secure and can sustain their lifestyle after the loss of an income earner.

Wealth Creation: Certain policies with savings and investment components help policyholders accumulate wealth or create a financial legacy.

Tax Benefits: Premiums paid and benefits received from most life insurance policies qualify for tax exemptions, adding to financial efficiency.

Loan Facility: Policies with cash value components allow the policyholder to borrow against accumulated savings, providing a source of emergency funds.

Retirement Planning: Annuity and pension-based life insurance help ensure continued income after professional retirement.

Child Education and Marriage Planning: Child plans secure funding for tuition or major life events.

Peace of Mind: Knowing that one’s family will be cared for in difficult times offers invaluable comfort.

Choosing a Life Insurance Policy

Selecting the right life insurance product requires careful consideration of individual needs, life stage, financial goals, risk appetite, and affordability of premiums. Factors like age, health condition, income, liabilities, dependents, and future expenses should be analyzed. For instance:

Young individuals with high earning capacity may opt for ULIPs or endowment plans for long-term savings and higher returns.

Those with fluctuating incomes may prefer universal life insurance for its flexible premium structure.

Families seeking pure risk cover at affordable rates may go for term insurance.

Older policyholders aiming for legacy planning could consider whole life or annuity plans.

How Life Insurance Works

After policy selection, the insured pays regular or one-time premiums. The insurer, in turn, commits to paying the sum assured if the event specified in the contract occurs. Beneficiaries must file a claim with required documentation—like death certificates and policy papers—for prompt settlement. Insurers usually process claims quickly but may reject those violating contract conditions.

Common Exclusions and Considerations

Life insurance contracts contain exclusions and limitations, such as suicide within a defined period, death from hazardous activities, war, or fraudulent claims. Clarity on specific events covered under the policy is vital to avoid disputes.